Page 46 - AA 2023 Year Book Website

P. 46

Syria

GENERALLY FAVOURABLE SOWING CONDITIONS, BUT HIGH

COSTS OF INPUTS HINDER AGRICULTURAL PRODUCTION

Sowing of winter wheat and barley kg in most governorates. For comparison,

crops, for harvest from May onwards, usu- the average nationwide price of 1 kg of

ally takes place between late September urea in October 2021 was SYP 2 100. Simi-

and December after seasonal rainfall re- lar increases were recorded for other fer-

plenish soil moisture. Although seasonal tilizers and crop protection material that,

rainfall across much of the country started despite their often unknown origin and

on time in September 2022, the amounts efficacy, remain available on the market,

were rather limited. The first significant but are not accessible for many farmers

rainfall of the 2022/23 cropping season with consequent low application rates

was recorded in November, with above Although the price of subsidized die-

average amounts in all governorates. sel remained unchanged at SYP 500/litre

December 2022 rainfall, however, was since 2021, it is unavailable at the subsi-

significantly lower than average across dized price due to fiscal difficulties. The

the country, with the largest differences average free market price of diesel for

in Al Hassakeh (the main cereal produc- transportation in September 2022 ranged

ing governorate) and southern parts of from SYP 950/litre in Al Hassakeh to over

the country. As of end December 2022, SYP 6 800/litre in Hama and Sweida. As

barley sowings were nearing comple- of November 2022, broad fuel shortages

tion, while about 60 percent of planned were reported across the country as a (during the period 2002 2011). At 300 000

winter wheat sowings were carried out direct result of the economic crisis, lead- tonnes, barley production is about 15 per-

under generally acceptable weather con- ing to a variety of fuel serving measures, cent of the bumper harvests gathered in

ditions. According to the latest seasonal such as reducing fuel allocations for gov- 2019 and 2020, and less than 40 percent

weather forecast for the December 2022 ernment vehicles, limiting the frequency of the pre crisis average.

February 2023 period, rainfall amounts of provision of the subsidized fuel for

are expected to be close to average in the private vehicles, and postponing sport- Despite the below average produc-

northeast (including Al Hassakeh), while ing events. In agriculture, fuel shortages tion, the cereal import requirement in the

below average precipitation amounts could constrain the ability of farmers to 2022/23 marketing year is forecast at 2.7

are expected in the northwest (including carry out mechanized operations. In ad- million tonnes, about the same as in the

Aleppo, an important cereal producing dition, combined with limited water avail- previous year, but 10 percent below the

governorate). In case of significant drier ability in transborder river flows coupled, five year average as ongoing economic

than average conditions, it would result in high fuel price may constraint farmers’ challenges and lack of foreign exchange

a third consecutive season affected by ir- ability to irrigate their crops in case of er- hamper the country’s ability to finance

regular rainfall. ratic rainfall. imports.

Following well below average harvests The quantity of wheat seeds provided After two years of below average har-

in 2021 and 2022, and coupled with the by the General Organization for Seed vests, elevated feed prices are increasing

effects of broad macroeconomic chal- Multiplication (GOSM) is generally not the cost of production for livestock farm-

lenges, farmers have limited financial sufficient to cover the national needs and ers. In August 2022, despite the recent

resources and access to formal credit re- farmers generally rely on the markets or conclusion of the harvest, average barley

mains very constrained, while prices of saved seeds for planting. prices reached almost SYP 2 300/kg, up

inputs further increased. over 40 percent compared to one year

earlier. At the same time, prices of live

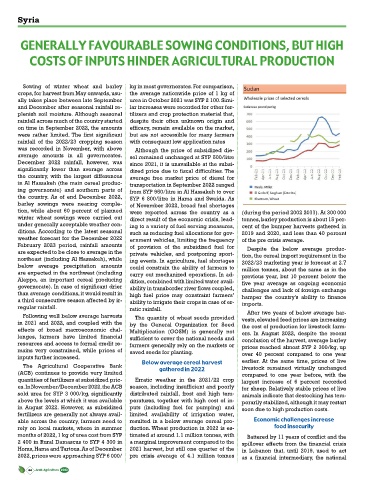

The Agricultural Cooperative Bank Below average cereal harvest livestock remained virtually unchanged

gathered in 2022

(ACB) continues to provide very limited compared to one year before, with the

quantities of fertilizers at subsidized pric- Erratic weather in the 2021/22 crop largest increase of 6 percent recorded

es. In November/December 2022, the ACB season, including insufficient and poorly for sheep. Relatively stable prices of live

sold urea for SYP 3 000/kg, significantly distributed rainfall, frost and high tem- animals indicate that destocking has tem-

above the levels at which it was available peratures, together with high cost of in- porarily stabilized, although it may restart

in August 2022. However, as subsidized puts (including fuel for pumping) and soon due to high production costs.

fertilizers are generally not always avail- limited availability of irrigation water,

able across the country, farmers need to resulted in a below average cereal pro- Economic challenges increase

rely on local markets, where in summer duction. Wheat production in 2022 is es- food insecurity

months of 2022, 1 kg of urea cost from SYP timated at around 1.1 million tonnes, with Battered by 11 years of conflict and the

2 400 in Rural Damascus to SYP 4 300 in a marginal improvement compared to the spillover effects from the financial crisis

Homs, Hama and Tartous. As of December 2021 harvest, but still one quarter of the in Lebanon that, until 2019, used to act

2022, prices were approaching SYP 6 000/ pre crisis average of 4.1 million tonnes as a financial intermediary, the national

44 Arab Agriculture 2023